The Middle-Income Trap: Speed is What you Need

The middle-income trap can be seen as rent-seeker capture, and speed is the key to getting out.

The middle-income trap is the problem of countries quickly rising out of relative poverty, but then getting stuck in the “middle-income zone,” which is variously defined as particular income ranges, or 50% of US GDP per capita. The economist estimates that only 23 countries have ever escaped it, and a suspicious number of those are petrostates or tax havens.

The usual explanation for this is that poor countries can initially grow quickly because there is low-hanging fruit in technological improvements, and low labor costs make them competitive in international markets. As the easy wins dry up and labor prices rise, though, they stagnate, unable to replicate what makes high-income economies so productive.

But why don’t they take some seemingly obvious wins like ease of doing business, education, and rule of law?

The global explanation is that it’s not that the easy economic wins are all taken; it’s that the easy political wins are gone.

Early improvements are win-win, in that there’s upside for everyone in improving basic infrastructure, sanitation, and safety, that is to say, they’re positive-sum. As time goes on, however, the necessary policy improvements will eventually upset some constituencies. If they’re powerful enough, though, they won’t allow the policy to proceed even if it would benefit the country overall.

Economic Historian Brad DeLong, when interviewed by Tyler Cowen, describes it:

A society where the returns to engaging in positive-sum … let’s win-win, figure out how to cooperate productively … are less than the returns from figuring out how to join some force-and-fraud, exploitation and domination machine.

The middle-income trap looks to me a lot like that thing expanding its reach.

This constituency would be called rent-seekers, or those who seek to enrich themselves without producing anything. They’re the bane of any economy, but will invariably show up as countries get richer, and the gains to extracting rather than producing improve.

However, there is a known antidote, and that is speed.

Speed is What You Need

By “speed” I mean the pace of economic growth. A country with ongoing, year-over-year growth in the upper single digits has at least has a chance of powering through the middle-income trap before it’s overwhelmed by budding rentiers. There are three reasons for this:

You need speed because fast growth makes the economy tilt positive-sum. The pie is growing quickly, so it’s comparatively attractive to try to grow with it, rather than build up an extractive apparatus to screw everyone else as a secondary actor. Capital and talent flow into high-growth sectors, whereas “in most countries, rent seeking rewards talent more than entrepreneurship does, leading to stagnation.”

The second is that rent seekers need time to first form coalitions to concentrate their power, and then even longer to insert their interests into the workings of governments and institutions. When the landscape is rapidly changing, who your allies are and the best way to interact with the economy is constantly in flux. A shoe-production license monopoly isn’t very useful when just a few years later everyone’s switched to making motorcycles.1

Finally, once high growth begins, it becomes a mandate to govern. Citizenry accustomed to getting richer every year demand this from governments, often forgiving other sins (like authoritarianism) in exchange. Governments feel existential pressure to keep delivering, so they continually check emerging cronyism before it can dampen growth. This was implicit with Deng Xiaoping, explicit with Park Chung-hee, and became part of the technocratic bargain for Lee Kuan Yew.

What Escape Looks Like

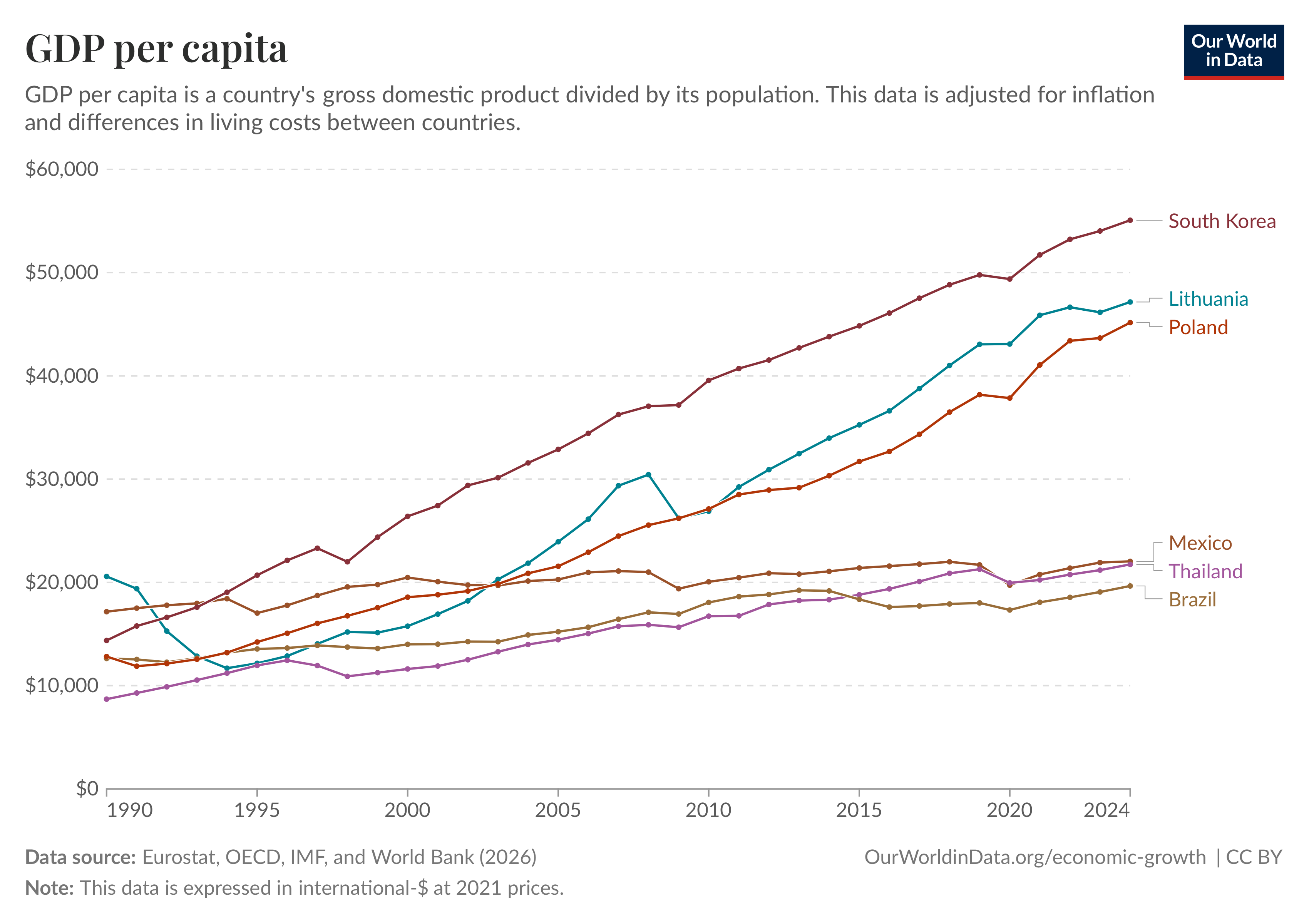

So does the data bear that speed predicts escape? If you look at the 43 countries that have spent recent time in the middle-income zone, two clear paths out of the trap emerge:

Path 1: High velocity (>5% per capita growth). South Korea, Taiwan, Japan, Singapore, Hong Kong, and Ireland. Possibly China, too, but time will tell. Speed alone was sufficient; the growth rate outran rentier consolidation.

Path 2: Moderate velocity (3.5-5%) + EU accession: Poland and Lithuania.2 Growth rates that were not sufficient on their own (Thailand and Malaysia had comparable rates and didn’t escape). What made the difference was the EU imposing binding institutional requirements: acquis communautaire, judicial reform, competition policy, anti-corruption frameworks, all incentivized by membership accession that had overwhelming domestic support.

There are some moderate growth close calls that still got trapped by rent-seeking, such as Malaysia and Brazil. Malaysia effectively codified rent-seeking into its constitution through mandated Bumiputera favoritism, while Brazil’s import-substitution regime allowed favored industrialists to grow rapidly and lock in rents simultaneously.

It could be said that very high early growth rates indicate an economy already has structural advantages to see it through the middle-income range. This is almost certainly true for newly commodity-rich countries that have become high-income, but places that were poor at midcentury were generally poor because they had no advantages to speak of.

Implications

First, the standard prescriptions, invest in education, build R&D capacity, improve competitiveness, and rule of law, mistake the symptoms for the disease. If you don’t address how decisions are made, these can never be effectively implemented. The binding constraint isn’t that the country can’t innovate; it’s that the people who benefit from non-innovation have veto power over reform.

Second, middle-income escapes may be more historically contingent than we hope, which is probably why they’re so rare. They’re helped by a combination of external discipline (Cold War security dependence, EU accession), growth as a governing mandate, and sheer velocity that outpaces the rent lock-in timeline.

Third, the speed thesis suggests a disturbing prediction about mature economies that have already escaped the trap. The mechanism that prevented rentier capture during high-growth periods doesn’t protect you once growth slows. Japan’s Lost Decades, and possibly the growing sclerosis of many Western economies, represent the same phenomenon at a higher income level: rent-seeking coalitions that were held in check by growth and now have nothing to restrain them.

(Perhaps we’ll soon start discussing the high-income trap.)

The trap is probably the natural state of political economy, so what requires explanation is why anyone makes it out. It seems that, briefly and under extraordinary conditions, they moved fast enough to get out before it snapped closed.

See The Rise and Decline of Nations for more on the effects of coalition formation.

What exactly qualifies a country as having been in the middle-income trap varies. Certain countries, such as the Czech Republic, Uruguay, and Estonia, have been left out because of their histories of wealth. As for Spain, Portugal, and Greece, historically, they have suffered from stagnation at high income, rather than getting stuck on their way from poor to rich.